Why Today’s Family Offices May Be Less Diversified Than They Think

And How a Risk-Managed, Liquid Strategy Can Protect Generational Wealth

The Hidden Concentration Risk

A recent Barron’s summary of a J.P. Morgan Private Bank survey of 333 global single-family offices (average net worth $1.6 billion) reveals something striking.

Despite rising geopolitical risk, inflation uncertainty, and market concentration, most family offices remain heavily allocated to:

- Large-cap public equities

- Private equity and venture capital

- Illiquid alternative investments

At the same time:

- 72% own no gold

- 89% own no crypto

- 50% own no hedge funds

In other words, many sophisticated investors are not meaningfully hedged.

They are simply long risk assets.

That distinction matters more today than at any point since 2008.

The Diversification Illusion

On paper, portfolios appear diversified:

Traditional holdings

- Public equities

- Private equity

- Venture capital

- Real estate

- “Alternatives”

Common risk exposures

- High valuation multiples

- Growth-dependent cash flows

- Long-duration assets sensitive to rates

- Equity beta

- Limited liquidity

But when you look under the hood, many of these assets share the same drivers.

When markets are rising, this structure feels diversified.

When markets fall, correlations rise quickly.

Private assets don’t protect — they simply mark down later.

The Liquidity Trap Since 2022

Private investments have historically offered attractive returns. But the post-2022 environment changed the math.

Family offices are now facing:

- Longer time to exits

- Delayed IPO windows

- Reduced M&A activity

- Secondary market discounts

- Capital calls during weak markets

This creates a structural problem.

Illiquid assets cannot be rebalanced or used defensively when risk rises.

You’re effectively locked in.

During periods of stress, the inability to reposition may matter more than the return profile itself.

Liquidity is not a convenience — it is a form of risk management.

What’s Missing: Active Risk Management

Most family offices are still operating with a traditional mindset:

“Own great assets and hold through cycles.”

That works — until valuation extremes, policy shifts, or geopolitical shocks create prolonged drawdowns.

Today’s environment features:

- Concentrated mega-cap markets

- Elevated P/S and CAPE multiples

- Rising global tensions

- Higher-for-longer interest rates

- Increasing volatility regimes

This is not a passive backdrop.

It’s a tactical one.

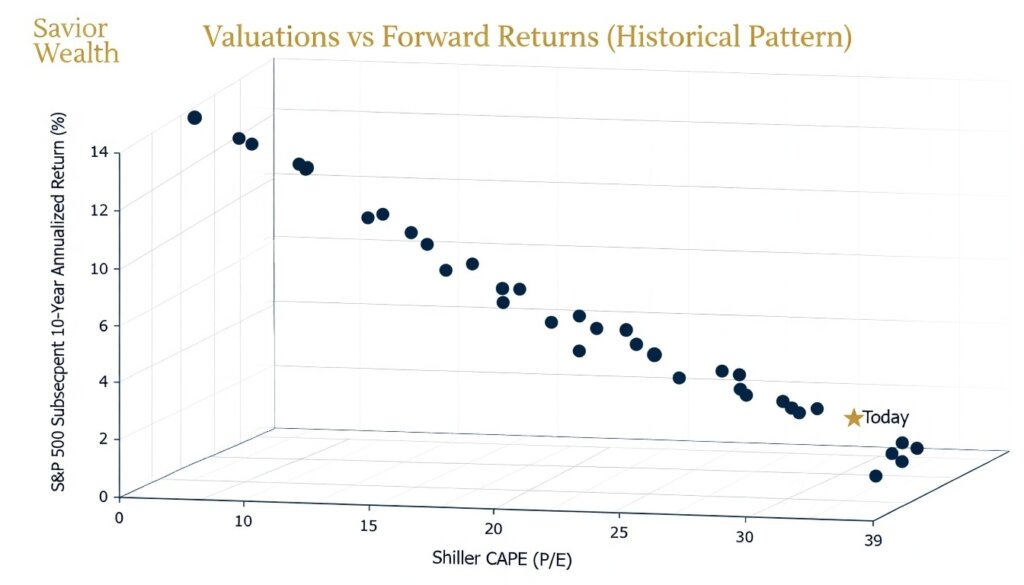

When valuations are extreme — like today with the Shiller CAPE near 39 — subsequent 10-year returns have historically been lower.

Where Savior Wealth Fits

Savior Wealth was built specifically to solve this gap.

Not to replace private investments.

Not to chase speculative hedges.

But to protect and stabilize a portion of family capital using a liquid, disciplined, risk-managed approach.

Our framework focuses on:

Liquidity First

Public, tradable instruments allow:

- Rapid repositioning

- Tactical hedging

- Downside protection

- Opportunistic buying

Capital stays flexible rather than locked.

True Diversification

We diversify across:

- Asset classes

- Factors

- Cycles

- Risk regimes

- Leveraged and inverse exchange-traded funds when appropriate

Active Risk Controls

Using both fundamental and technical analysis, we:

- Reduce exposure during elevated risk periods

- Increase protection when markets become fragile

- Deploy defensive or inverse strategies when appropriate

- Seek smoother return paths

By pairing illiquid long-term growth holdings with a liquid risk-managed allocation, families gain optionality, smoother returns, and the ability to weather difficult markets without forced selling.

The goal is simple:

Preserve capital.

Compound steadily.

Protect generational wealth through every market cycle.

The Savior Market Conviction Compass

Rules-based risk management indicators provide a framework for assessing conviction levels in risk assets through valuation, credit, and breadth indicators.

Remaining Conviction Level: 60/100 — cautious but still constructive risk backdrop.

Higher scores mean greater conviction to own risk assets.

Lower scores mean risk-management takes priority.

The goal isn’t to beat every bull market.

The goal is to preserve capital, compound steadily, and avoid large drawdowns that permanently impair wealth.

A “Stability Sleeve” for Family Offices

Many families find the most effective structure is:

- Core private holdings (long-term growth)

- Illiquid alternatives (strategic)

- Savior Wealth liquid risk-managed sleeve (capital protection + flexibility)

This sleeve acts as:

- Shock absorber

- Liquidity reserve

- Tactical allocator

- Rebalancing engine

When markets dislocate, this capital is available — not trapped.

The Strategic Advantage

In uncertain markets, the most valuable asset isn’t necessarily higher returns.

It’s optionality.

Liquidity + risk management = optionality.

Families who maintain a protected, liquid allocation can:

- Meet capital calls without selling at lows

- Rebalance into dislocations

- Fund opportunities others cannot

- Sleep better during volatility

That is real diversification.

The Bottom Line

Many family offices are sophisticated — but still structurally concentrated.

Heavy exposure to:

- Mega-cap equities

- Private markets

- Illiquid alternatives

creates hidden risk when cycles turn.

Adding a liquid, actively managed, risk-aware strategy isn’t about abandoning growth.

It’s about protecting what has already been built.

At Savior Wealth, we focus on helping families:

Preserve capital.

Manage risk.

Stay liquid.

And compound through every cycle.

Because wealth that survives downturns is wealth that lasts generations.

Working With Family Office Investment Teams

Many family offices outsource portions of their portfolio to specialized managers.

Savior Wealth frequently partners alongside:

- CIOs

- Investment committees

- OCIO platforms

- External asset managers

We are typically engaged for 5–20% of assets to provide a complementary liquid, risk-managed allocation that enhances resilience without disrupting existing strategies.

Call to Action

If your family office would benefit from adding a liquid, risk-managed allocation designed to protect capital and enhance flexibility, we welcome a confidential discussion.

Schedule a consultation with Savior Wealth to evaluate how a Stability Sleeve may strengthen your portfolio resilience.

About the Author

Todd M. Ingwersen, CFP®, CIMA®, CEPA®

Founder | Chief Investment Officer | Savior Wealth

Todd leads Savior Wealth’s investment strategy and risk-management process. With more than two decades of experience advising successful families and business owners, he specializes in capital preservation, tax-aware portfolio construction, and disciplined market cycle management. Savior Wealth integrates fundamental research, technical analysis, and rules-based risk controls to help clients protect and compound wealth across full market cycles.

Disclosures

This content is provided for informational and educational purposes only and does not constitute individualized investment advice, a recommendation, or an offer to buy or sell any security. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Leveraged and inverse ETFs involve additional risks and may not be suitable for all investors. Clients should carefully review applicable prospectuses and consult their advisors before investing.