Leverage Then and Now: More Than History, It’s a Modern Reality

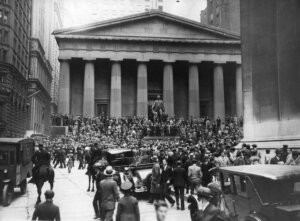

The 1929 stock market crash is often used as a history lesson in financial risk. What turned a routine market correction into a sweeping collapse was, in large part, the role of leverage. Nearly a century on, leverage remains deeply woven into the financial system but in more varied—and often less visible—forms.

How Regulation Changed Leverage After 1929

At the time of the Great Depression, investors could frequently purchase $10 of stock with only $1 of their own capital. Call loans and loosely monitored margin accounts fueled this speculative excess. In the aftermath, regulation permanently reshaped market structures. Today, under Regulation T, most investors can borrow up to 50% of a stock’s purchase price—meaning $1 of equity supports about $2 of exposure, rather than $10. This aimed to reduce the systemic risk of extreme leverage, particularly among retail investors.

Modern Leverage Is More Complex

Leverage didn’t disappear with new rules; it adapted. While classic margin borrowing remains, modern markets utilize a spectrum of leverage tools, including:

- Traditional margin accounts

- Securities-based lending (SBL)

- Options and derivatives

- Leveraged ETFs

- Corporate debt and other forms of financial engineering

- Expanded household and government borrowing

Much of today’s leverage does not feel speculative—even to borrowers. For instance, securities-based lines of credit (SBL) are often marketed as tools for liquidity or personal finance planning, not as leverage for trading. Yet the underlying risk remains: a decline in portfolio values can trigger forced actions similar to margin calls, sometimes catching investors off guard.

The Surge in Securities-Based Lending (SBL)

SBL has grown rapidly over the last decade. Investors use these credit lines for various purposes—funding property purchases, educational expenses, or lifestyle needs—while avoiding the need to sell appreciated assets. As markets rise, so does the urge, and ability, to borrow. The risk emerges when markets fall: lenders may require additional collateral, principal paydowns, or liquidate holdings at inopportune times. Even investors who believed they were managing risk conservatively can find themselves exposed to downward market pressure.

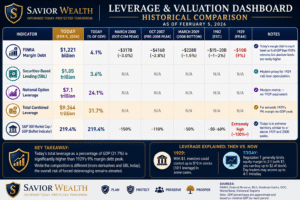

Why Leverage and Valuation Together Matter

High leverage alone rarely triggers market instability. But when leverage coincides with periods of elevated valuations, the system becomes more fragile. In such environments, small disruptions can have amplified effects—exacerbating both price gains and losses.

What Investors Should Watch

- Leverage levels: Watch growth in margin debt, securities-backed loans, and other borrowing across both households and corporations.

- Market valuations: Elevated asset values combined with high leverage deserve extra vigilance.

- Credit spreads and volatility: Widening spreads or increased volatility can signal stress points where leverage may amplify moves.

Investors should be aware that leverage can facilitate liquidity and economic growth for long periods, but can also intensify volatility during periods of market stress. Monitoring leverage structures is about understanding how the broader market might respond, not about predicting precise outcomes.

Practical Takeaways for Investors

At Savior Wealth, our ongoing research monitors leverage, valuations, and other key signals as part of our disciplined investment process. The current environment, while not signaling maximum risk, underscores the importance of:

- Diversification and prudent portfolio construction

- Conservative liquidity and cash management

- Active, deliberate oversight of individual and system-wide leverage

Our goal is to help investors stay resilient regardless of market conditions.

Additional Reading

- San Francisco Fed – Margin Requirements as a Policy Tool

- FINRA – Securities-Backed Lines of Credit Explained

- Federal Reserve – Background and Summary of Regulation T

Disclosure

This material is for informational and educational purposes only and should not be construed as investment, legal, or tax advice. Past performance does not guarantee future results. Market conditions and leverage dynamics can change rapidly. Investors should consult their financial advisor regarding their specific circumstances.

Summary

This Savior Wealth Insight discusses leverage margin risk 1929 vs today and how investors can think about risk,

valuation, leverage, liquidity, and disciplined portfolio construction.

The article is educational and designed to help readers understand important market risks without making short-term predictions.

Generated: 2026-05-16

Research Context and Data Sources

The Compass uses a rules-based process that incorporates market data, macro data, valuation data,

credit conditions, volatility, and market internals.

Use the Compass Two Ways

Subscribe to the Compass

For investors who want ongoing market interpretation, weekly updates, and deeper dashboard commentary.

Private Discovery Session

For qualified families and business owners interested in becoming a Savior Wealth client rather than managing this alone.

Important Disclosures

This material is for informational and educational purposes only and should not be considered individualized

investment advice, a recommendation to buy or sell any security, or a guarantee of future results.

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results.

Market indicators are imperfect, may change quickly, and should be evaluated within the context of an investor’s

objectives, time horizon, liquidity needs, risk tolerance, and overall financial plan.

Savior Wealth does not provide tax or legal advice. Please consult your tax, legal, or other professional advisor

regarding your specific circumstances.

Additional disclosures are available here:

https://www.saviorwealth.com/important-disclosures/