Understanding an “Expensive” Market: Price, Value, and Expectations

For years, investors and headlines have warned that the market is “expensive.” Sometimes those warnings prove prescient, but often, markets defy them and keep climbing. The famous 1996 speech by Alan Greenspan about “irrational exuberance” came well before the dot-com peak. Internet and semiconductor stocks soared for years before the cycle turned. This reveals a simple truth: valuation can highlight when expectations are high, but it does not provide a reliable countdown clock for market turns.

“Valuation is not a clock. It is a measurement of how much future success is already priced in.”

What Do Investors Mean by “Expensive”?

When advisors or investors label the market or a stock “expensive,” they typically mean its price is high relative to its underlying fundamentals—earnings, sales, book value, cash flow, or future growth. But expensive does not mean a sudden reversal is imminent. Similarly, a “cheap” asset may stay ignored or underperform for long stretches.

Section 1: Price Is Not Valuation

A $20 stock can be expensive, while a $500 stock can be cheap. Price alone says little. Investors use tools like price-to-earnings ratio (P/E), forward P/E, price/earnings-to-growth (PEG), price/sales, price/book, EV/revenue, EV/EBITDA, free cash flow yield, and trends in revenue growth or returns on equity to determine how much optimism—or skepticism—is already reflected in the price.

Section 2: Expensive Means Expectations Are High

High valuation ratios typically mean investors have confidence the company will achieve outsize growth, high margins, or defend a dominant position. If the firm outperforms these expectations, the stock can continue to climb. But if reality simply meets, or falls below, those lofty hopes, prices can quickly reset.

Consider the lesson from Scott McNealy, CEO of Sun Microsystems, after the dot-com bust. The company traded at about 10 times revenues at the peak, an extreme valuation. In retrospect, McNealy questioned what investors expected at that price: “What were you thinking?” Even tremendous companies may disappoint if you pay for perfection up front.

Similarly, Cisco—one of the champions of the internet era—took nearly two decades to regain its old highs after investors overpaid in 1999–2000. The business survived and matured, but the starting valuation made for a challenging ride.

Section 3: Cheap Means Expectations Are Low

Value stocks trade at lower multiples—low expectations are already priced in. These stocks may only require an improvement in sentiment or earnings to outperform. But “cheap” can also reflect legitimate risks: country-specific uncertainty, poor management, slowing growth, or structural headwinds.

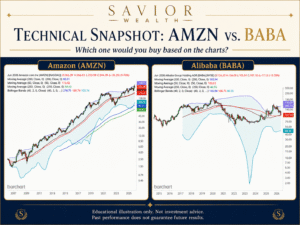

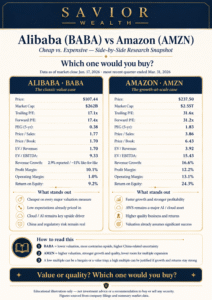

A useful illustration is Alibaba (BABA) versus Amazon (AMZN)—not as a recommendation, but as a framework. As of this writing, BABA trades at much lower valuation multiples than AMZN. Alibaba has a depressed price/earnings (P/E), price/sales, price/book, and EV/EBITDA, making it a classic “value” profile with low expectations and more upside if sentiment improves. Conversely, Amazon justifies its high multiples with stronger growth, higher returns on equity, robust cloud leadership, and institutional trust. The trade-off: AMZN = Higher Quality, BABA = Better Value. Investors must choose what matters more in each case—expected return from recovery, or stability and predictability.

Section 4: Momentum and Sentiment Matter in the Short Term

Markets are not solely mathematical. In the near term, emotion, liquidity, positioning, technical patterns, and narrative dominate. Over the long run, companies’ revenue, profitability, free cash flow, and business durability take over.

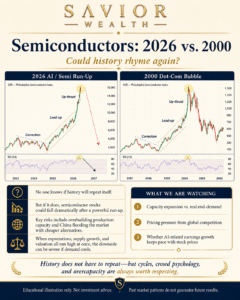

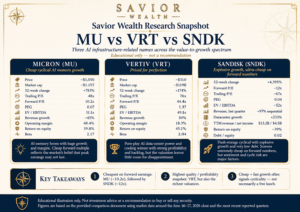

Semiconductors are a recent case study. In the late 1990s, chipmakers rode a wave of internet and PC demand. In this decade, the AI infrastructure surge (think: specialized memory from Micron, AI data center backbones from companies like Vertiv) has driven valuations higher still. When revenue and earnings are booming, high prices may be justifiable—temporarily. But remember: if supply catches up or demand shifts, today’s high multiples can correct with surprising speed.

Section 5: What Makes the Stock Market Expensive?

At the market level, analysts use composite signals such as Shiller’s CAPE ratio, market price-to-sales, market cap to GDP, prevailing profit margins, and interest rates to gauge valuation. Concentration in a handful of mega-cap companies and the level of earnings growth assumed are also crucial.

It’s worth repeating—the Savior Market Conviction Compass includes valuation, but that’s only one input. Breadth, trend strength, credit health, volatility, leverage, sentiment, and macroeconomic factors are all just as important for risk management.

Section 6: The Right Question for Investors

“The better question is not whether something is expensive. The better question is: What has to happen for today’s price to make sense?”

Rather than asking, “Is this expensive?” ask, “What is already priced in?” and “What must happen for this valuation to be justified?” For any stock or the market:

- How rapidly must revenue grow?

- How high do margins need to go?

- How long can growth last?

- How much competition or disruption is on the way?

- What happens if expectations fall short?

Private markets, from SpaceX to AI innovators like OpenAI and Anthropic, reinforce this caution. When investors stake huge private-market values based on outsized future visions, they’re effectively making a bet on decades of exceptional growth. If the outcome falls short, valuations can reset dramatically. Recent trends in AI and cloud show that falling model prices and cost competition can boost adoption—but may compress profit margins, raising tough questions about who will capture long-term value.

Even giants like Apple are not immune—rising input costs (e.g., memory, chips, supply chain shocks) can pressure profit margins. If those costs cannot be passed on, earnings could disappoint; if passed on, demand must absorb the difference.

Conclusion: Valuation as Risk/Reward, Not a Crystal Ball

Expensive markets can keep rising as long as expectations are exceeded. Cheap stocks can remain cheap until sentiment shifts or risks subside. Great companies can be lackluster investments if you pay too much for future perfection. Conversely, unloved firms can prove rewarding if reality modestly improves upon low expectations.

Valuation should not be used as a short-term timing tool. Instead, let it guide your risk and reward assessments. At Savior Wealth, our focus is not predicting each market move, but understanding what is priced in, where optimism or pessimism is most pronounced, and whether the risk investors take is justified by expected reward.

“Great companies can be bad investments if investors pay too much for them.”

Important Disclosures: This material is for educational and informational purposes only. It is not a recommendation to buy, sell, or trade any security. Securities cited are examples for discussion only. Savior Wealth and its representatives may hold the securities or ETFs discussed. Investing involves risk, including loss of principal. Past performance does not guarantee future results. International investments involve political, regulatory, currency, liquidity, and geopolitical risks. Private-company valuations are uncertain and may not reflect public market liquidity or risk.

Research Context and Data Sources

The Compass uses a rules-based process that incorporates market data, macro data, valuation data,

credit conditions, volatility, and market internals.

Use the Compass Two Ways

Subscribe to the Compass

For investors who want ongoing market interpretation, weekly updates, and deeper dashboard commentary.

Private Discovery Session

For qualified families and business owners interested in becoming a Savior Wealth client rather than managing this alone.

Important Disclosures

This material is for informational and educational purposes only and should not be considered individualized

investment advice, a recommendation to buy or sell any security, or a guarantee of future results.

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results.

Market indicators are imperfect, may change quickly, and should be evaluated within the context of an investor’s

objectives, time horizon, liquidity needs, risk tolerance, and overall financial plan.

Savior Wealth does not provide tax or legal advice. Please consult your tax, legal, or other professional advisor

regarding your specific circumstances.

Additional disclosures are available here:

https://www.saviorwealth.com/important-disclosures/